The Evolution of SR&ED Eligibility

Reference Article (>5 Years Old)Please note that the information herein may be outdated, links could be inactive, and policies discussed may have evolved. For the most current data, consult our latest publications. If you would like us to refresh this article as it is of interest to you, please contact us. |

At SREDucation, we’re taking the time to document all of the changes that have occurred to the SR&ED program over the years. In our “From the Archives” series, you’ll be able to see how the program has evolved since its inception in 1986.

Interpretation Bulletin IT-439 and the Birth of Experimental Development

While the Scientific Research & Experimental Development (SR&ED) program didn’t exist as we know it today until 1986, prior to this the government was still grappling with how to define “scientific research.” Before 1985, whether or not work could be considered “applied or basic research” or “development” was outlined in Interpretation Bulletin IT-439; however, taxpayers complained that the definitions provided therein weren’t helpful. In response to this, the Department of Finance amended the bulletin to include the term “experimental development” in order to solidify that routine development was not SR&ED-eligible. “With respect to the general guidelines,” the Department of Finance said, “this department is in basic agreement with the approach being taken, namely that to qualify for the research and development tax incentives, an activity must embody some scientific or technological advancement, have some elements of scientific or technological uncertainty, and be carried out in a systematic and organized fashion.”

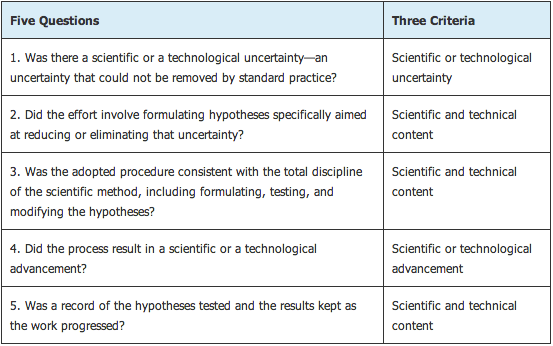

The Three Criteria and the Five Questions

In 1986, a new information package was created titled Information Circular 86-4 Scientific Research and Experimental Development. This document laid out the three criteria of SR&ED eligibility:

- Scientific or technological advancement: The search carried out in the experimental development activity must generate information that advances your understanding of the underlying technologies.

- Scientific or technological uncertainty: Technological obstacles / uncertainties are the technological problems or unknowns that cannot be overcome by applying the techniques, procedures and data that are generally accessible to competent professionals in the field.

- Scientific and technical content: A systematic investigation entails going from identification and articulation of the scientific or technological obstacles/uncertainties, hypothesis formulation, through testing by experimentation or analysis, to the statement of logical conclusions.

The three criteria have remained a pillar of SR&ED since this time. However, in 1998, a landmark SR&ED court case—Northwest Hydraulic Consultants Ltd. v. The Queen—outlined a new eligibility system that has very recently been worked into SR&ED documents (e.g., the T661[13]): the five questions.

The Five Questions vs. The Three Criteria

Today, the five questions are the first thing Canada Revenue Agency (CRA) reviewers ask when examining a SR&ED claim.

This article is based on a page on the CRA website: A brief history of the guidance on the eligibility of work.