“There is no need to re-learn existing lessons.” – Our SR&ED Consultation Response (March 2024)

Background

The Department of Finance published a new statement on January 31, 2024, “Government launches consultations to increase Canadian research and development and intellectual property retention“. In this statement, the Government of Canada announced that they have launched consultations on how to improve support for research and development, and how to create and retain intellectual property in Canada. This statement marks the beginning of the long-awaited review of the Scientific Research and Experimental Development (SR&ED) program.

Our organization, with a rich history providing consulting services and researching the program, brings forth recommendations and insights based on extensive experience and a comprehensive analysis of the program’s impact and evolution.

Our SR&ED Consultations Response

(1a) How can the SR&ED program remain effective in supporting R&D investment by businesses of all types in Canada?

Bottom Line Up Front (BLUF):

We recommend that the CRA:

- does continue to provide the SR&ED program as a neutral investment tax credit program (i.e. no change).

Background:

One of the key features of the SR&ED program is that allows for a broad range of companies across many fields of science and technology to apply. There 147 distinct fields of science and technology codes for form T4088.[1] The most recent update indicates that upwards of 20,079 claims were processed in FY2022-2023, representing 17,013 individual claimants.[2] This has allowed businesses of all types in Canada to apply, so long as they meet eligibility requirements. By continuing to offer this program without narrowing the scope further, the program can continue to support businesses of all types in Canada.

(1b) How can the SR&ED program better support the growth and success of R&D-intensive Canadian businesses going forward?

BLUF:

We recommend that the CRA:

- improve the predictability of the program;

- continuously improve education and outreach through tools such as the Self-Assessment and Learning Tool (SALT), public seminars, educational videos, and industry-specific outreach;

- improve written communication, including re-introducing the two-letter system, and

- enhance CRA My Business Account by making it easier for company program administrators.

Background:

On March 28, CPA Canada posted a video to YouTube video of an interview and webinar they co-hosted with the CRA to review updates to the SR&ED Investment Tax Credit (ITC) Program.[3] This session covered an overview of the program results from 2023 and highlighted the upcoming initiatives that will be undertaken by the CRA to enhance program efficacy in 2024. The co-hosts were Susan Bishop (Chair of CPA Canada’s SR&ED Tax Advisory Committee, and member of CPA’s Tax Advisory Group), and Lorraine Redekop (Director General of the SR&ED program). Updates included plans to continue education and outreach, through public seminars, educational videos, and other mediums. This includes continuing education via tools such as the Self-Assessment and Learning Tool (SALT), in addition to ongoing seminars on the program. It did not address sector-specific guidelines or educational videos, but these have been part of the program historically. Overall, this is a positive approach, and we encourage the CRA to continue to make the program more predictable for applicants through continued education and outreach.

One of the questions posed to the CRA in the video was whether a return to a “two-letter” system to advise claimants of their status would be considered. The service standard is to process claims that are accepted as filed within 60 days, but there is often minimal to no communication once filed. In the past, there were separate letters for companies acknowledging receipt and providing guidance, which some taxpayers indicated increased predictability. Ms. Redekop, stated in the update video that the CRA was willing to revisit this idea. This is one of many small but effective ways the CRA can increase predictability for applicants.

We recommend the CRA to continues to improve their accessibility; namely, the ability for companies to contact them directly if they have questions. This includes re-building support programs that create relationships with Research and Technology Advisors (RTAs), making it easy for taxpayers to receive updates by phone, and creating and promoting the online portal mentioned in the update video. Increasing direct access will improve predictability and will likely have a spillover effect of enabling taxpayers to either circumvent or minimize their use of consultants.

(2a) What improvements to the definition of SR&ED […] should be considered?

BLUF:

We recommend that the CRA:

- does not modify the definition of the SR&ED program, as this will negatively impact predictability and deviate from internationally recognized definitions;

- does consider clarifying the distinction between innovation and R&D; and

- does consider any changes completed in a parallel program, such as the patent box.

Background:

The definition of SR&ED currently aligns closely with internationally accepted definition from The Organisation for Economic Co-operation and Development (OECD):

Research and experimental development (R&D) comprise creative and systematic work undertaken in order to increase the stock of knowledge […] and to devise new applications of available knowledge.[4]

By contrast, innovation is defined in the Oslo Manual “Guidelines for Collecting, Reporting and Using Data on Innovation” (2018) as:

Innovation is production or adoption, assimilation, and exploitation of a value-added novelty in economic and social spheres; renewal and enlargement of products, services, and markets; development of new methods of production; and the establishment of new management systems. It is both a process and an outcome.[5]

The definition of R&D is fairly standard, outlining an approach (creative and systematic work) and the output (increase in knowledge); the definition of Innovation is vague and self referencing, as “both a process and an outcome”. Other definitions of innovation are similarly unstable. In her PhD thesis Scientific Research and Experimental Development (SR&ED) Engagement and Management by Small Canadian-Controlled Private Corporations (CCPCs), Lucille Perreault lists several other definitions, including:

Schumpeter (1934) asserts that innovation is the creation of new combinations of existing resources and forces. Schumpeter’s definition allows for a broad spectrum of innovation, such as the combination of adding email and internet functionality to the traditional functions of a phone. Rogers (2003) avers that innovation is an idea, process, or item that someone perceives as new. This definition, however, is quite vague as the perception of new is fairly subjective. Other definitions are more specific. Damanpour (1996, p. 694) defines innovation as “a new product or service, new process technology, new organization structure or administrative systems, or new plans or programs pertaining to organization members… Rosenberg (1982) differentiates between product and process innovation: a product innovation is the development of a new product or service, while a process innovation is an innovation that does not change the production or delivery of an existing product or service, but rather creates a new or improved method of production or delivery. [6]

Given the lack of agreement regarding “innovation” and the lack of focus on knowledge or IP generation, this term is less preferable to the internationally-recognized OECD definition of R&D. Further, any changes to the definition will cause issues with predictability. We would therefore suggest that any changes to be completed in a parallel program, such as the proposed patent box, or through other targeted programs.

(2b) What improvements to […] the program’s eligibility criteria […] should be considered?

BLUF:

We recommend that the CRA:

- investigate the reasoning behind the minimum threshold for eligible expenditures in Quebec, to determine relevance at the federal level;

- investigate if there are ways to simplify claiming material costs, or whether retiring these expenses and accounting for them elsewhere is preferable, and

- investigate the value of continuing to allow for two methods (proxy and tradition), with the focus on the value and overhead burden of the traditional method.

Discussion:

In 2014 the Quebec government quietly announced two changes to their R&D tax credits, the most notable of which was the introduction of minimum eligible expenditure thresholds (Section 2.1.1). Their reasoning was as follows:

“Currently, many business claim tax credits for small amounts of expenditure, for example, in 2011:

— 40% of businesses that claimed R&D tax credits had eligible expenditures of less than $50 000, for an average expenditure of about $25 000 per business;

— 40% of businesses that claimed the tax credit for investments relating to manufacturing and processing equipment had eligible expenditures of less than $12 500, for an average expenditure of about $4 500 per business.

[…] the administration of all these claims entails considerable administrative costs for the government and businesses. In some cases, the administrative costs related to claiming the tax credit can be higher than the tax assistance granted.”[7]

The minimum eligible expenditure thresholds for R&D tax credits as a whole became:

- $50,000 for corporations with assets equal to or less than $50 million

- $225,000 for corporations with assets $75 million or more

- An amount that increases linearly between $50,000 and $225,000 for corporations with assets between $50 million and $75 million

Rather than conducting a duplicate investigation, consider working with peers at Revenue Quebec (RQ) to determine if similar issues exist at the federal level, whether the RQ changes had a positive impact (over 10 years), and whether similar changes make sense in this context.

Additionally, in our experience and as noted in responses, an area that results in a higher administration cost for all parties is allocating material expenditures. When the CRA conducts reviews of a taxpayers ITCs, if they have materials costs, it is our experience that discussions regarding what is “part of the body of the thing” takes up considerable time relative to its importance. As an example, we recently supported a small farming group; during the review, a disproportionate amount of time was spent discussing the “materials” that are part of the testing process, while that represented <5% of the costs. It would be interesting to calculate the ITCs related to material expenditures, as well as the challenges associated with recapture rules if the materials transformed go on to become a commercial product. These statistics are not currently reported publicly.

Removing materials expenditures would not require a complete change to policy but could be accomplished (relatively cost-neutrally) with the retirement of the Materials for SR&ED policy, with some minor adjustments in other policies to show the elimination of those costs towards qualified expenditures.[8] There is precedent for this changes: the CRA did something similar in 2012 when they eliminated both lease expenditures and capital expenditures. While they haven’t “archived” these policies, they have updated them to show that those costs after a certain date no longer apply.[9]

These suggestions are provided with a caution: while the overall material costs claimed across Canada are likely very small compared to salary/wage costs, their removal would still have negative impacts for certain SR&ED claimants, specifically those in manufacturing, etc. because their work revolves around the use of materials to prototype new/improved products or processes. As an example, a company in Ontario with nearly 200K in material costs would lose out on 84K in SR&ED ITCs. Material costs are directly involved in the SR&ED work performed, so a cautious approach is recommended. It may be that with better communication, the difficulties with material costs in reviews could be avoided.

Finally, it is currently unclear how many companies use the traditional method as opposed to the proxy method. Using rough math based on publicly available information, if $1.2B of the ITCs (out of $3.6) are going to software, as reported for 2023, that means at least 1/3 don’t use the proxy method; the same likely holds true for the other ~1/3 of claims for Electrical Engineering. It may be worth reviewing the relative benefits vs. the administrative overhead of keeping the two-method system (proxy & traditional). Again, this suggestion is provided with a caution: it will be worth investigating the impact prior to implementing any changes.

(2c) What improvements to […] the overall architecture should be considered?

BLUF:

We recommend that the CRA:

- provide more clarity around the current architecture of the SR&ED program.

Discussion:

This question is difficult to answer without knowing the current architecture. Some changes that were announced via CPA Canada update are good, such as the national workload model whereby claims are now assigned to SR&ED specialists based on their field of expertise rather than the region the claim originates from.[10]

3 How does the SR&ED program complement the existing suite of support programs for R&D in Canada? How could this complementarity be improved?

BLUF:

We recommend that the CRA:

- adjust SR&ED risk measurements to account for scrutiny through other technology funding programs (ex. IRAP), to reduce duplication of efforts;

- provide better examples of key concepts, such as how to pro-rate expenditures and track them between programs; and

- provide better explanations of how the SR&ED program works in conjunction with other programs.

Discussion:

As previously noted, the SR&ED ITC program is neutral, so any company that meets the criteria can apply. The government therefore mainly allows market conditions to decide what projects are considered, thereby reducing crowding-out of market-driven R&D projects.[11] Ideally, the SR&ED program should maintain its neutral position, as there are many other targeted programs currently in effect that complement the existing suite of support programs for R&D in Canada. These include, but are not limited to:

- Clean Energy Investments: A 15% Investment Tax Credit worth approx. ~$2 billion per year ($25.7 billion through 2035).[12]

- Artificial Intelligence: $2.4 billion through a variety of mechanisms, including an additional $200 million delivered through NRC IRAP.[13]

As discussed in the CPA Canada update[14], better alignment with other programs (ex. IRAP) would be helpful for all parties, to reduce issues such as under-claiming other funding or failing to claim SR&ED due to the misperception they can only apply for one program. Other methods to further improve complementarity, include:

- Many years ago, IRAP projects that focused on technology development were subjected to less scrutiny, as the belief was that the NRC counterparts conducted similar due diligence. While there are areas that the current IRAP program covers that would be excluded from SR&ED (for example, user experience and market research), it may be worth putting together a taskforce to identify and communicate areas of alignment to all stakeholders (CRA, NRC, taxpayers, and tax preparers) and see if the administrative burden can be lessened.

- Similarly, better examples of how to pro-rate expenditures and track them between programs would be appreciated. The CRA put out an excellent paper on how to align COVID funding programs with SR&ED, which affected many taxpayers. Considering that IRAP supports over 22,000 firms (funded and unfunded)[15], companies and there are 17,000 SR&ED claimants, there is a high degree of likelihood that companies are submitting claims to both programs. It would be advisable given the overlap to provide more guidance on how this should be structured, to address the under-reporting issues cited by the CRA.[16]

- More generally, better explanations and examples of how to combine SR&ED with other programs would be beneficial for all stakeholders. There is a pervasive misconception that taxpayers can only apply for one program at a time, which is incorrect.

4 Are there more effective ways in which the overall level of assistance provided within the SR&ED program could be targeted? If so, what changes could be made to the SR&ED program to offset the costs of any proposed enhancements?

BLUF:

We recommend that the CRA:

- align support for large and small firms more closely with the spillover benefits they generate;

- considers expanding the eligibility and potentially adjusting the rates for Canadian Controlled Public companies, and

- enhance existing programs (ex. IRAP) that provide more support for smaller, early-stage/higher risk projects.

Discussion:

The ultimate objective of the SR&ED program is to raise the economic well-being of Canadians. The program is achieving this objective, but its effectiveness could be improved. Unfortunately, the upcoming review is focussed on issues that will have, at best, a minor impact on the net social benefit of the program. The best way to improve the effectiveness of the SR&ED investment tax credit is to align support for large and small firms more closely with the spillover benefits they generate.[17]

One of the common phrases of the last few years is “follow the science”. There is a growing body of research that suggests a reconsideration of the support for small versus large firms. In Tax Support For R&D And Intellectual Property: Time For Some Bold Moves, Lester (2022) states several controversial recommendations that he believes are required for improving the SR&ED program, along with sound reasoning. These include:

Governments in Canada subsidize R&D performed by small firms at a much higher rate than R&D performed by larger firms. The combined federal-provincial investment tax credit rate is approximately 20 percent for large firms compared to about 43 percent for smaller firms (Box 1). The huge gap in subsidy rates would be justified if spillovers from small firms were greater than those from larger firms. The evidence, however, suggests the opposite. Kim and Lester (2019) report that R&D performed by large firms generates spillovers that are almost three times greater than those generated by small firms.14

As discussed in Lester (2021), the misalignment of subsidy and spillover rates is the main reason why investment tax credits for small firms fail a benefit-cost test while their large firm counterparts result in a substantial net benefit. Taking into consideration spillovers and the other factors, such as compliance costs, that affect the net social benefit (see the online appendix), the large firm tax credit rate that maximizes the net social benefit is 2 ½ times greater than the optimal credit rate for smaller firms. Rebalancing the SR&ED tax credit by reducing the rate for small firms and increasing it for large firms would therefore raise the net social benefit of the R&D subsidy. [18]

In the footnotes, Lester further clarifies that “large firms generate 52 cents in spillovers for each dollar spent on R&D, while the spillover rate for small firms is 19 percent.” [19] Recently (2022), the C.D. Howe Institute penned an open letter on this topic:

Theory and limited empirical evidence suggest that spillovers are higher for basic/applied research, so the subsidy rate should also be higher.

Second, as I have discussed elsewhere, the SR&ED tax credit could be substantially improved by rebalancing support for small and large firms. Combined with provincial measures, the tax credit for small firms is 39 percent, compared to 19 percent for large firms. In addition, about 2,000 small firms top up the SR&ED incentive with targeted assistance from the federal Industrial Research Assistance Program (IRAP), raising the subsidy rate to almost 60 percent on average for these firms.

The huge gap in subsidy rates between large and small firms would be justified if spillovers from small firms are greater than those from larger firms. The evidence, however, suggests the opposite. Setting both rates at 25 percent would raise the net social benefit of the SR&ED program per dollar of tax revenue forgone. Small firms with particularly promising R&D projects would continue to benefit from IRAP, bringing their overall subsidy rate to about 45 percent.

Rebalancing the rates would also improve Canada’s innovation performance. Subsidies lower the hurdle rate for private investment, which allows R&D projects with less commercial potential to go ahead. Excessive subsidies therefore reduce the share of R&D-intensive products that are brought to market.”[20]

It is our recommendation that the CRA consider this research when reviewing the benefits of the ITC rates for larger and small firms, and consider instead working with their peers in other departments to enhance existing programs (ex. IRAP) that provide more support for earlier-stage and higher risk projects. The added benefit is that many complementary programs have more regular payouts; this financial structure for government funding is preferable and addresses some other cashflow concerns expressed by taxpayers.

5 How can the SR&ED program effectively ensure the retention of intellectual property (IP) within Canada, particularly to support innovative Canadian businesses to remain Canadian-owned and operated?

BLUF:

We recommend that the CRA:

- measure and promote the spillover benefits from this program, ensuring clarity of messaging;

- implement payback requirements for sale of Canadian SR&ED-funded IP to other countries; and

- allow access to preferential SR&ED rates for all small-medium enterprises regardless of whether they are privately or publicly controlled.

Discussion:

If we look at news coverage, the current definition of success in Canadian business appears to be acquisition by a large, often US-based firm. Given that the programs are funded with the objective contributing to the overall social and economic wellbeing of Canadians (via spillover benefits), making it easier to keep SR&ED dollars and IP in Canada is preferable.

The focus should be on Canadian ownership and benefits; implementing payback requirements if they are purchased by another country would enable the continued funding of the program. This needn’t be an impediment to acquisition; particularly for emerging leaders AI, cybersecurity, and energy efficiency it would be an additional calculation in the purchase formula. Similar conditions currently exist in other investment vehicles (such as low cost, conditionally repayable loans) where policy requirements for acquisitions can be replicated and aligned.

Additionally, it may be worth reconsidering perceptions regarding private vs public companies. A 2021 article titled Reversing the Decline of the Canadian Public Markets, from two University of Alberta profs, Bryce Tingle and Ari Pandes, details how public companies grow faster, create more IP and are more likely to stay Canadian:

Companies that stay private are, on average, less successful, less productive, less likely to grow into national champions, and more likely to be sold to foreign buyers […] Public companies grow faster, grow larger, become both more productive and efficient, and have cheaper access to capital. An IPO permits early investors to exit while allowing managers to continue to build the company.”[21]

Similarly, Pierre Lortie at the C.D. Howe Institute highlights Canada’s difficulty in scaling-up companies. They recommend that Canadian public companies should be eligible for refundable SR&ED credits:

High-growth and innovative Canadian companies lose most of the benefits of the federal SR&ED credits program when they go public, but not if they are privately financed. This bias of federal fiscal policy is counterproductive. Canadian public companies should be eligible for the SR&ED program in the same way as Canadian-controlled private corporations of comparable size and stage of development.”[22]

In light of the above, it is worth reconsidering our perception of private vs. public small and medium enterprises and whether the benefits of increasing the ITCs available and their structure (refundable or non-refundable, enhanced or regular) would be beneficial.

If you are seeing this sentence, this article has been republished without authorization from The InGenuity Group. If you would prefer to support the content creator, please view original articles at https://www.sreducation.ca/articles/

6 How can the SR&ED program be improved and streamlined to make it easier for entrepreneurs to access support?

BLUF:

We recommend that the CRA:

- clarify the target market of the program and focus outreach programs on those organizations;

- review prior research and efforts to achieve similar goals for improvement;

- clarify what is required in terms of supporting documentation and eligible tracking methods;

- provide training materials in advance, so that the framework for productive discussions are in place; and

- ensure a clear method is available to track progress, whether through a portal or a direct point of contact.

Background

A recurring theme in industry feedback, whether private (via conversations with taxpayers), public (on LinkedIN), or in our survey was the need for certainty and timeliness of payments, concurrent with reducing costs (time and monetary) of compliance. Put simply, addressing these issues will ensure it is easier for entrepreneurs to access support as they will choose to apply, rather than avoid an unpredictable and cumbersome program.

We urge caution with any changes to this program. Historically, significant changes and increases to the complexity of the system creates an environment of fiscal uncertainty, which discourages companies from applying for SR&ED. The program has already gone through some of these challenges. For example, in 1994 the 18-month filing deadline was introduced. Many businesses panicked and submitted applications, resulting in “the bulge” – the number of claims and processing times increased dramatically, as illustrated in this graphic:

Image of Average Processing Times Attributable to CRA for Referred SRED Claims[23]

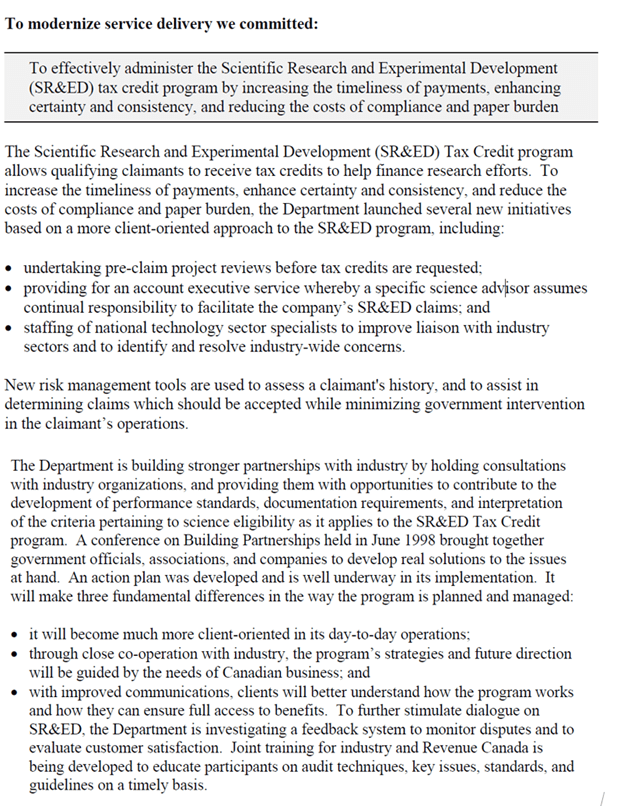

To address the high processing times, volume of complaints, and deteriorating relationship between the CRA and claimants, a minister’s conference (called “Building Partnerships”) was held in Vancouver in June 1998. The SR&ED industry discussed the program with the government in an attempt to make the program work effectively. In late 1998, a 13–point action plan based on the recommendations heard at the conference was released. The 1998-99 CRA Report to Parliament – which sought to address those recommendations – could have been written in the last year:[24] Effectively, many of the challenges are perennial, as demonstrated below:

Image taken from 1999 CRA Report to Parliament

Thus, there are valuable lessons that can be (re)learned from reviewing prior service improvement documents. For example, up until the retirement of IC86-4R3 in 2012, there were a number of sector-specific guidelines. Some of these were particularly important, given the volume of claims submitted annually. For example, in the CRA update via CPA Canada, the statistics indicate that upwards of 1/3 of claims are for software.[25] Despite this, there are currently minimal documents on this topic, that most recent of which was a PowerPoint presentation: Eligibility of Work in SR&ED Projects Containing Software Development (2017). Previously, there were carefully crafted Information Circulars, designed in consultation with industry, including IC97-1 – Scientific Research and Experimental Development – Administrative Guidelines for Software Development. This carefully written 15-page document that provided critical guidance to those claiming an advancement in Software Development and the retirement of this form concurrent with new, generalized policies created unnecessary confusion. A return to this client-centered approach with sector-specific guidance for the top fields of science and technology would be cost-effective, targeted support that would enhance the program while “minimizing government intervention in the claimant’s operations” – a noble goal in 1998, as well as today.

Additionally, the CRA has announced they are working on an online portal regarding SR&ED; while this is a laudable use of technology, it should not distract from other communication initiatives that will improve the program. Something as simple as being accessible by phone is critical, as demonstrated this recent (2024) Tax Court of Canada Ruling:

The Applicant had a fiscal year end of June 30, 2018. Their accounting firm filed their tax electronically on December 5, 2019, without any SR&ED forms filled out. The CRA issued a notice of assessment on December 11, 2019. The Applicant’s accountant filed an amended return with the SR&ED information on December 20, 2019. The accounting firm attempted to follow up with the CRA in early 2020 but they were unable to reach anyone in the CRA about the return. In December 2020, the Applicant learned that the CRA could not locate their 2018 SR&ED claim. Their accountant sent a letter on their behalf to the CRA on January 21, 2021, explaining that a SR&ED claim had been filed in December of 2019 and no response had been received. The letter did not contain a notice of objection or a request for an extension of time. On March 8, 2021, the Applicant received news from the CRA that their claim was denied as it was filed more than 12 months after the return date was due. On April 9, 2021, the Applicant’s accountant filed a formal Notice of Objection which the CRA notified the Applicant on June 2, 2021, that it could not be accepted as the deadlines had passed. The Judge ruled that although an error was committed by the CRA, the requirement to file a Notice of Objection and an extension request in the prescribed timeline established by the Income Tax Act stands. The case was dismissed without costs.[26]

This case could have had a different outcome if information had been available from the CRA in a timely manner regarding the status of the SR&ED application. I would again draw your attention to the CRA Report to Parliament (1999):

[..] with improved communications, clients will better understand how the program works and how they can ensure full access to benefits. To further stimulate dialogue on SR&ED, the Department is investigating a feedback system to monitor disputes and to evaluate customer satisfaction. Joint training for industry and Revenue Canada is being developed to educate participants on audit techniques, key issues, standards, and guidelines on a timely basis.[27]

Other suggestions include:

- provide better guidance on what is considered acceptable supporting documentation. For most other tax items (ex. childcare tax benefits) the CRA indicates what must be on the receipts. There is only high-level guidance for supporting documentation, which forces companies to seek out external guidance (i.e. through hiring SR&ED consultants);

- send training materials regarding the SR&ED program in advance of a review / audit, so companies have time to prepare. Currently, the in-review presentations are effectively useless, as they do not allow the taxpayer time to review the information and come prepared; and

- clarify where and when the allocation method is considered acceptable. The CPA Canada update with the CRA, a comment was made a comment about costs being estimated. Currently, time allocations are considered a valid method per the Salaries or Wages policy; this should be made explicit, as there is confusion amongst taxpayers and CRA Research and Technology advisors.

7 How can your suggested enhancements be funded by existing support available through the SR&ED program? What potential changes could best focus support to benefit Canada, including by creating economic opportunities for Canadians?

First, there is no need to incur new costs and re-learn existing lessons. Many of these lessons have been documented repeatedly since 1986, with the CRA committing to addressing them each time. Second, research suggests that minor, strategic changes and guardrails can generate the spillover benefits and income to help sustain the program and justify its existence.

Finally, we strongly urge caution with major changes but encourage continuous improvement.

Continuous improvement will enable the enhancements through existing support; however, the reliability and stability of the SR&ED program is the simplest way to focus support that benefits Canada and creates economic opportunities for Canadians.

Download our full response: InGenuity Group Response to CRA Consultation on SR&ED – April 2024

Connect With Us!

Share your thoughts by commenting below or joining the conversation on our LinkedIn page, Facebook page, or via Twitter.

REFERENCES

[1] The Government of Canada (2020). “T4088 – Scientific Research and Experimental Development (SR&ED) Expenditures Claim – Guide to Form T661.” Accessed April 15, 2024 from: https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4088/guide-form-t661-scientific-research-experimental-development-expenditures-claim-guide-form-t661.html#toc30

[2] Bishop, S. and Redekop, L. (2024) 2024 CRA Update on SR&ED Program. (YouTube and Webinar) Accessed April 2, 2024, retrieved from: https://www.youtube.com/watch?v=-OBZmJAeUnY

[3] Bishop, S. and Redekop, L. (2024) 2024 CRA Update on SR&ED Program. (YouTube and Webinar) Accessed April 2, 2024, retrieved from: https://www.youtube.com/watch?v=-OBZmJAeUnY

[4] OECD (2015) “Frascati Manual 2015: Guidelines for Collecting and Reporting Data on Research and Experimental Development. The Measurement of Scientific, Technological and Innovation Activities.” Accessed March 21, 2024 from: https://www. oecd-ilibrary.org/docserver/9789264239012-en.pdf?expires=1650549718&id=id&accname=guest&checksum=FC4F 77B2B2063768E1BED8A71552644C.

[5] OECD (2018) “Oslo Manual 2018: Guidelines for Collecting, Reporting and Using Data on Innovation, 4th Edition.” Accessed March 21, 2024 from: https://www.oecd.org/innovation/oslo-manual-2018-9789264304604-en.htm

[6] Perreault, L. (2020). Scientific Research and Experimental Development (SR&ED) Engagement and Management by Small Canadian-Controlled Private Corporations (CCPCs) (dissertation) Accessed April 12, 2024 from: https://carleton.ca/profbrouard/wp-content/uploads/ThesisPhDLucilletPerreault202101.pdf

[7] Finances Québec, Update on Québec’s economic and financial situation Fall 2014 (Page D.38). Retrieved April 12, 2024 from: http://www.finances.gouv.qc.ca/documents/Autres/en/AUTEN_updateFall2014.pdf

[8] The Government of Canada (December 18, 2014). “Materials for SR&ED Policy.” Retrieved April 12, 2024 from: https://www.canada.ca/en/revenue-agency/services/scientific-research-experimental-development-tax-incentive-program/materials-policy.html

[9] The Government of Canada (December 18, 2014). “SR&ED Lease Expenditures Policy.” Retrieved April 12, 2024 from: https://www.canada.ca/en/revenue-agency/services/scientific-research-experimental-development-tax-incentive-program/lease-expenditures-policy.html

[10] Bishop, S. and Redekop, L. (2024) 2024 CRA Update on SR&ED Program. (YouTube and Webinar) Accessed April 2, 2024, retrieved from: https://www.youtube.com/watch?v=-OBZmJAeUnY

[11] Crowding out is the economic theory that argues that rising public sector spending drives down or even eliminates private sector spending

[12] Department of Finance Canada. (2023, March 28). Government of Canada releases Budget 2023. Canada.ca. Accessed April 15, 2024 from: https://www.canada.ca/en/department-finance/news/2023/03/government-of-canada-releases-budget-2023.html

[13] Securing Canada’s AI advantage. (2024, April 7). Prime Minister of Canada. Accessed April 15, 2024 from: https://www.pm.gc.ca/en/news/news-releases/2024/04/07/securing-canadas-ai

[14] Bishop, S. and Redekop, L. (2024) 2024 CRA Update on SR&ED Program. (YouTube and Webinar) Accessed April 2, 2024, retrieved from: https://www.youtube.com/watch?v=-OBZmJAeUnY

[15] National Research Council Canada. (2022, October 11). Summary Report – Evaluation of the NRC’s Industrial Research Assistance Program. Accessed April 15, 2024 from: https://nrc.canada.ca/en/corporate/planning-reporting/summary-report-evaluation-nrcs-industrial-research-assistance-program

[16] Bishop, S. and Redekop, L. (2024) 2024 CRA Update on SR&ED Program. (YouTube and Webinar) Accessed April 2, 2024, retrieved from: https://www.youtube.com/watch?v=-OBZmJAeUnY

[17] Lester, J. (2022). Tax support for R&D and intellectual property: Time for some bold moves. In Trusted Policy Intelligence [E-Brief]. Retrieved April 12, 2024 from: https://www.cdhowe.org/sites/default/files/2022-07/E-Brief_330_0718_0.pdf

[18] Lester, J. (2022). Tax support for R&D and intellectual property: Time for some bold moves. In Trusted Policy Intelligence [E-Brief]. Retrieved April 12, 2024 from: https://www.cdhowe.org/public-policy-research/tax-support-rd-and-intellectual-property-time-some-bold-moves

[19] Lester, J. (2022). Tax support for R&D and intellectual property: Time for some bold moves. In Trusted Policy Intelligence [E-Brief]. Retrieved April 12, 2024 from: https://www.cdhowe.org/public-policy-research/tax-support-rd-and-intellectual-property-time-some-bold-moves

[20] J. Lester Broadening the new review of tax support for R&D (2022) C.D. Howe Institute. Accessed April 15, 2024 from: https://www.cdhowe.org/intelligence-memos/john-lester-broadening-new-review-tax-support-rd

[21] Bryce C. Tingle, QC and J. Ari Pandes, “Reversing the Decline of Canadian Public Markets,” The University of Calgary SPP Publications Volume 13:14, April, 2021, Accessed April 12, 2024 from: https://journalhosting.ucalgary.ca/index.php/sppp/article/view/69444

[22] Lortie, P. & Daniel Schwanen. (2019). Entrepreneurial Finance and Economic Growth: A Canadian Overview. C.D. Howe Institute Commentary, 536 (2), p .20. Retrieved November 14, 2024 from: https://www.sreducation.ca/wp-content/uploads/Entrepreneurial-Finance-and-Economic-Growth-A-Canadian-Overview-SREDucation.ca_.pdf

[23] Lance, E. (2021, December 5). Analysis: Trends in SR&ED – processing times, number of claimants, value. SR&ED Education and Resources. Accessed April 15, 2024 from: https://www.sreducation.ca/report-data-trends-observed-sred-claims/

[24] Revenue Canada (1999). “Performance Report” pg. 40-41. Canadian Government Publishing – PWGSC. ISBN: 0-660-61022-1.

[25] Bishop, S. and Redekop, L. (2024) 2024 CRA Update on SR&ED Program. (YouTube and Webinar) Accessed April 2, 2024, retrieved from: https://www.youtube.com/watch?v=-OBZmJAeUnY

[26] The InGenuity Group (2024). “FOOi Inc. v. The King (2023).” Accessed April 15, 2024 from: https://www.sreducation.ca/legal-rulings-table-contents/fooi-inc-v-the-king-2023/ (Full ruling available from: https://decision.tcc-cci.gc.ca/tcc-cci/decisions/en/item/521192/index.do)

[27] Revenue Canada (1999). “Performance Report” pg. 41. Canadian Government Publishing – PWGSC. ISBN: 0-660-61022-1.